Captive insurance is a concept that has gained considerable attention in recent years, offering organizations a unique opportunity to take control of their insurance needs. With the ever-evolving landscape of risk management, businesses are seeking alternative strategies to mitigate potential financial impact. And this is where captive insurance comes into play.

Irs 831b Tax Code

At its core, captive insurance involves the creation of a subsidiary insurance company by a parent organization, effectively allowing it to self-insure. Through this approach, businesses can tailor their coverage to meet specific needs, safeguard against market fluctuations, and minimize reliance on traditional insurers. It provides a means for organizations to take charge of their risk management, enabling greater flexibility and control over the management of insurance-related costs.

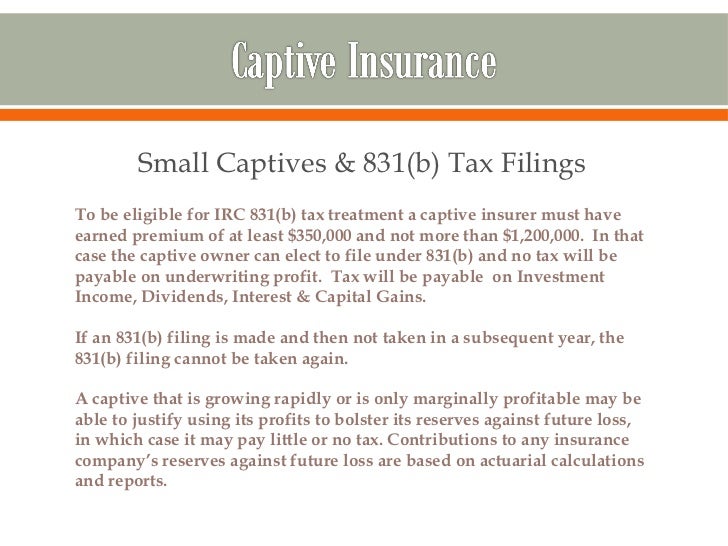

One prominent example within the realm of captive insurance is the IRS 831(b) tax code, which specifically addresses small insurance companies. Referred to as microcaptives, these entities can take advantage of certain tax benefits, resulting in potentially significant financial advantages for qualifying organizations. By exploring the intricacies of this tax code and understanding its implications, businesses can unlock a range of benefits that can positively impact their bottom line.

As we delve deeper into the world of captive insurance, we will explore the various strategies and structures available to businesses, shedding light on its potential advantages and considerations. From examining different types of captives to understanding the regulatory landscape surrounding this insurance mechanism, we will navigate the complex terrain of captive insurance and showcase the value it can bring to organizations across industries. Join us as we unlock the potential of captive insurance and uncover the benefits it holds for those willing to embrace innovative risk management solutions.

Understanding Captive Insurance

Captive insurance refers to a unique insurance arrangement where a company creates its own insurance company to cover its own risks. This alternative risk management strategy allows businesses to have more control over their insurance policies and potentially access a range of associated benefits.

In the world of captive insurance, one specific provision often comes into play: Section 831(b) of the IRS tax code. Under this section, qualifying small insurance companies, known as microcaptives, may elect to be taxed only on their investment income rather than their underwriting profits. This tax advantage can make captive insurance a particularly attractive option for certain businesses.

By establishing their own captive insurance company, businesses can gain greater flexibility in terms of coverage options and policy terms. This can be especially beneficial for companies operating in industries with unique risks or facing difficulties obtaining affordable or comprehensive coverage from traditional insurers.

Overall, captive insurance provides an opportunity for companies to take a more proactive approach to managing their risks. From cost savings to tailored policies, this alternative risk management strategy allows businesses to leverage their expertise and gain a deeper understanding of their own risk profile.

Leveraging the Benefits of 831(b)

When it comes to captive insurance, the 831(b) tax election holds tremendous potential for businesses seeking to maximize their insurance strategies. Under the IRS 831(b) tax code, eligible businesses can create a "microcaptive" or small captive insurance company to secure several advantages.

Firstly, utilizing the 831(b) election allows businesses to enhance their risk management capabilities. By establishing their own captive insurance company, businesses can tailor coverage to their specific needs, ensuring that no potential risks are left unaddressed. This level of customization enables greater control over their insurance program, resulting in comprehensive coverage that aligns precisely with their unique risk profile.

In addition to enhanced risk management, businesses leveraging the 831(b) tax election also benefit from potential tax advantages. The tax benefits of a captive insurance arrangement under 831(b) can be significant, as income generated by the captive is often taxed at lower rates compared to traditional insurance arrangements. This tax efficiency provides businesses with an opportunity to generate significant cost savings while at the same time ensuring their insurance needs are met.

Furthermore, captives utilizing the 831(b) election can accumulate wealth over time through the retention of underwriting profits. Unlike with traditional insurance, where excess premiums paid are typically lost, captives can retain profits from underwriting, investment income, and interest. This ability to accumulate wealth allows businesses to build financial reserves that can be utilized for future claims, reinvestment, or even distribution as dividends to shareholders.

In conclusion, taking advantage of the 831(b) tax election can unlock several benefits for businesses exploring captive insurance strategies. From tailored risk management solutions to potential tax advantages and the ability to accumulate wealth, the 831(b) election provides an avenue to optimize insurance programs to fit the specific needs and goals of businesses.

Navigating IRS Requirements

When it comes to captive insurance strategies, it is crucial to navigate and comply with the requirements laid out by the IRS. One of the key sections in the tax code that captive insurance falls under is 831(b). This tax code specifically pertains to small insurance companies and provides certain benefits for captive insurance arrangements.

The IRS 831(b) tax code allows captive insurance companies to be taxed on only their investment income, rather than their premium income. This tax advantage can be an attractive incentive for businesses looking to establish a captive insurance arrangement. However, it is important to note that to qualify for the benefits outlined in the tax code, certain requirements must be met.

One significant requirement is the level of risk that the captive insurance company assumes. To qualify for the tax benefits, the captive must demonstrate that it is a bona fide insurance company and not merely a tool for tax avoidance. The captive must also have adequate capitalization and operate in a manner consistent with insurance industry standards.

Additionally, the IRS requires annual reporting and compliance with various regulations for captive insurance companies. This includes maintaining proper documentation, filing annual tax returns, and cooperating with any IRS examinations or audits. Non-compliance with these requirements can lead to the loss of tax benefits and potential penalties from the IRS.

Understanding and navigating the IRS requirements is crucial for businesses considering captive insurance strategies. Working with knowledgeable professionals who specialize in captive insurance and tax compliance can help ensure that all necessary steps are taken to meet the IRS guidelines and maximize the benefits of captive insurance arrangements.